Favia Investment Group | Market Insights

Los Angeles Multifamily Cap Rates 2026: What West LA Deals Are Actually Trading At

By Don Favia | Updated March 14, 2026

https://www.faviainvestmentgroup.com/market-insights/los-angeles-multifamily-cap-rates-2026

Los Angeles Multifamily Cap Rates 2026: What West LA Deals Are Actually Trading At

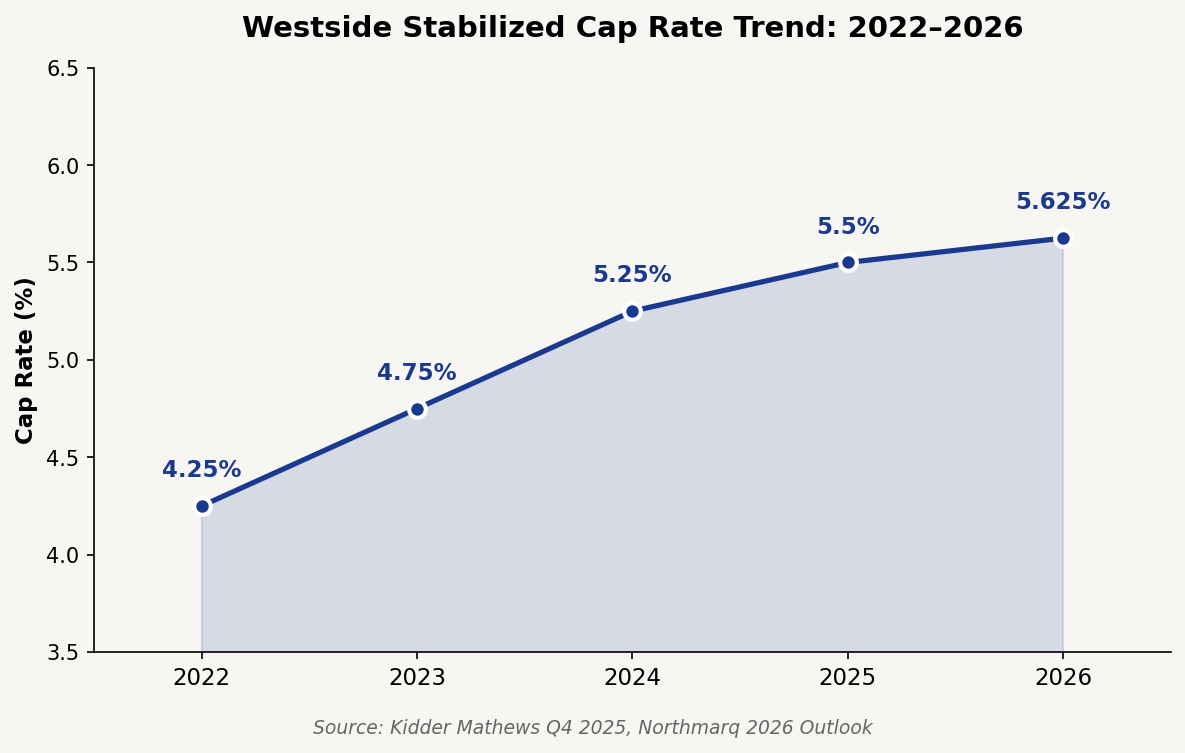

The LA metro average cap rate hit 5.7% in Q4 2025, up 60 basis points year over year. On the Westside, it has already moved further. Here is what deals are actually trading at in Q1 2026.

I have spent 20 years selling apartment buildings on the Westside of Los Angeles. Over $370M in career transaction volume, 850+ units, 100+ deals. Here is what I am seeing in actual deals right now, not from a research desk, but from the offers, counteroffers, and closing statements crossing my desk in early 2026.

Where Cap Rates Stand Right Now

The most recent published data shows the LA metro average cap rate at 5.7%, up 60 basis points year over year.[2] That is the published number. In Q1 2026, the conditions that drive cap rate expansion have not improved. They have gotten more pronounced.

Rents are declining. Supply is accelerating. Financing costs remain elevated. Every one of those factors pushes cap rates higher, not lower. Q4 2025 published data could be a floor, not a ceiling.

On the Westside specifically, stabilized assets are trading between 5.5% and 5.75%. Value-add deals trade tighter, between 4.75% and 5.25%. Those buyers are paying up because they see a rent growth play. GRMs across the Westside land between 11.0 and 14.5.[6]

The spread between submarkets is where the real story lives.

A 4.3% cap in West LA and a 5.5% cap in Westwood are not the same market. One buyer is chasing yield near UCLA. The other is buying durable cash flow in a supply-constrained corridor. Both are rational. The pricing logic is completely different.[3]

Why Cap Rates Keep Expanding Into 2026

Three forces are driving cap rate expansion, and none of them are reversing this quarter.

Rents are falling, not holding. This is the part most owners have not fully processed yet. Santa Monica median rent in March 2026 is $2,318, down 7.5% year over year, the steepest annual decline among all 27 cities tracked in the LA metro.[5] Month over month, Santa Monica rents fell 2.3% in March alone, accelerating from a 0.5% decline in February. The wildfire displacement demand that briefly lifted rents in 2025 has reversed. Rents are down 1.2% across the metro on the year.[5]

Buyers are already adjusting what they will pay.

Record new supply is hitting. Los Angeles is set to complete 12,300 new apartment units in 2026, the largest annual delivery on record, surpassing the 9,000 units delivered in 2025.[7] LA ranks fifth nationally for 2026 completions. On the Westside specifically, Palms and Mar Vista face over 2% inventory growth, among the highest in the metro.[7] New buildings leasing up with concessions pull rents down on the older stock nearby.

Debt maturity math is forcing decisions. CMBS and bridge loans originated at sub-4% rates during 2020 to 2022 are coming due.[4] Refinancing at today's rates is painful for most of those borrowers. Selling at today's cap rates, while uncomfortable for owners anchored to 2021 valuations, produces a better outcome than carrying a new loan at a substantially higher basis for another three years waiting for conditions to improve. That is not changing this quarter.

The RSO Change That Affects Every Westside Owner

LA City Council voted 12-to-2 in January 2026 to revise the RSO formula, effective July 1, 2026.[8] The maximum annual allowable rent increase drops from 8% to 4%. The minimum drops from 3% to 1%. The CPI basis is cut from 100% to 90%.

What this means practically: the long-run rent growth ceiling for RSO units on the Westside just got lower. Buyers are penciling in lower rent growth. That compresses what they will pay.

For the period June 1, 2025 through June 30, 2026, allowable RSO increases are capped at 3% for units where notice was not previously served.[8] Non-RSO units built before January 1, 2005 fall under AB 1482, which caps increases at 8% for 2026 (5% plus CPI of 3%).[8]

If you own a rent-stabilized building on the Westside, you have a narrowing window before buyers fully reprice the long-run income ceiling downward. For a full breakdown, read our LA rent control guide.

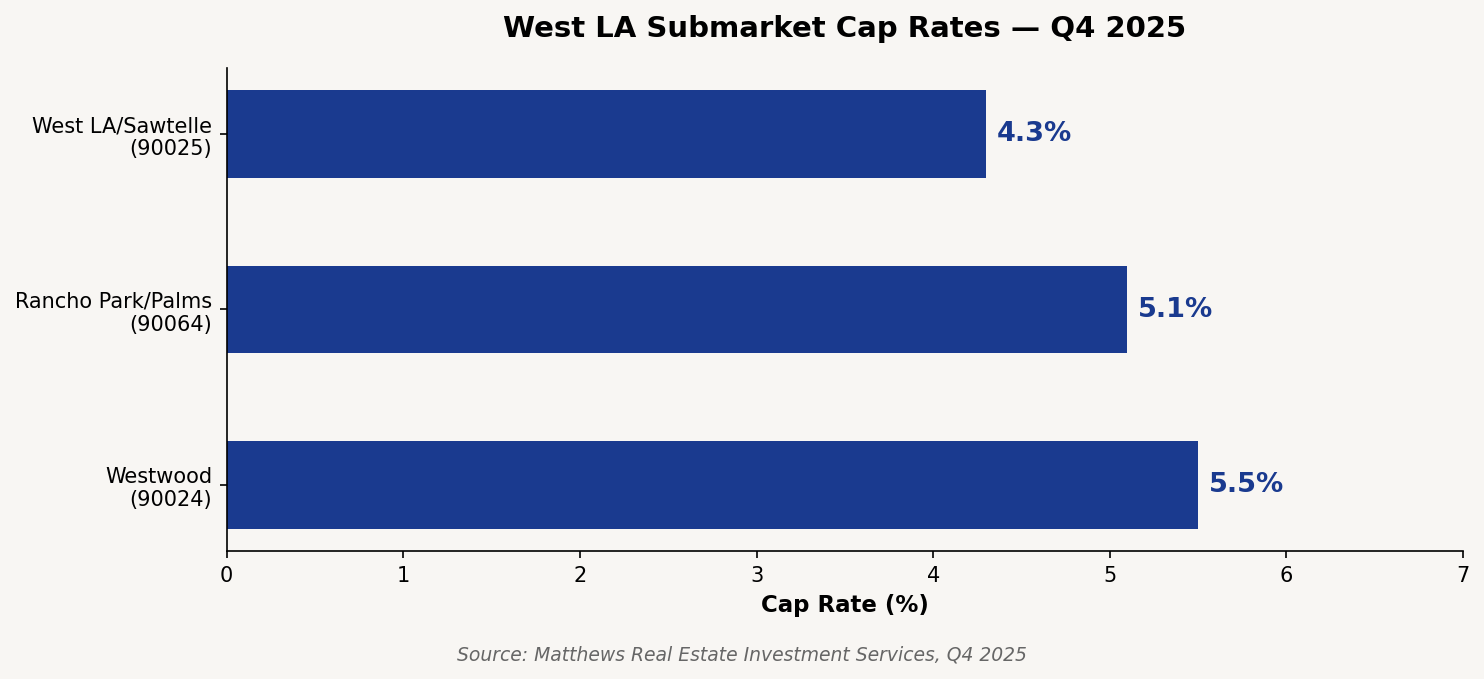

Submarket Breakdown

Every zip code on the Westside has its own pricing story. Here is what Q4 2025 data shows, with Q1 2026 context layered in.[3]

West LA / Sawtelle (90025): 4.3% cap rate. The institutional corridor. Expo Line access and Century City employment create durable rental demand. Buyers here are typically 1031 exchange capital seeking Westside yield.

Rancho Park / Palms (90064): 5.1% cap rate. Palms faces over 2% inventory growth from new supply in 2026.[7] Sellers here who are thinking about 2026 or 2027 should weight the new supply impact carefully. Lower entry points attract a wider buyer pool. Deals are getting done, but the competitive landscape shifts as new units absorb.

Westwood (90024): 5.5% cap rate. Larger institutional-scale product near UCLA. The elevated cap rate reflects asset size and buyer return requirements, not distress. UCLA keeps vacancy low. That gives Westwood some cushion from what is happening to rents elsewhere on the Westside.

The Rate Cut You've Been Waiting For Isn't Coming

A lot of Westside owners have been sitting on the sideline since 2023 with the same thesis: wait for the Fed to cut rates, watch cap rates compress, sell into a stronger market.

Here is what actually happened. The Fed did cut rates multiple times through 2024 and 2025, bringing the federal funds rate all the way down to 3.5%-3.75%. Then in January 2026, they stopped.[9] And LA multifamily cap rates expanded 60 basis points anyway.[2]

Rate cuts did not rescue valuations. They never do cleanly. Too many other things get in the way: local supply, rent trends, what lenders are actually willing to do. Right now every one of those is working against Westside owners.

Now layer in what is happening this week. There is an active war with Iran. Gas prices are up. Inflation was already elevated before the war started.[9] The war has made it worse. The CME FedWatch tool is pricing in near-zero probability of a rate cut at the upcoming March meeting.[10]

Mark Zandi, chief economist at Moody's: "Fed officials will sit on their hands until they get some clarity around how the war with Iran is playing out. That could take weeks, if not two to three months."[10]

Goldman Sachs has penciled in exactly one 25 basis point cut for all of 2026. December at the earliest.[11]

If your plan is to wait for a rate cut before you sell, you are looking at late 2026 at the absolute earliest, with no guarantee that a single 25 basis point cut does anything meaningful to Westside valuations. Meanwhile NOI is eroding, new supply is coming online, and the RSO rent ceiling just got cut. The math gets harder every quarter you hold.

The sellers who do well in 2026 are not the ones waiting for a turnaround. They are the ones who price correctly for where things actually are.

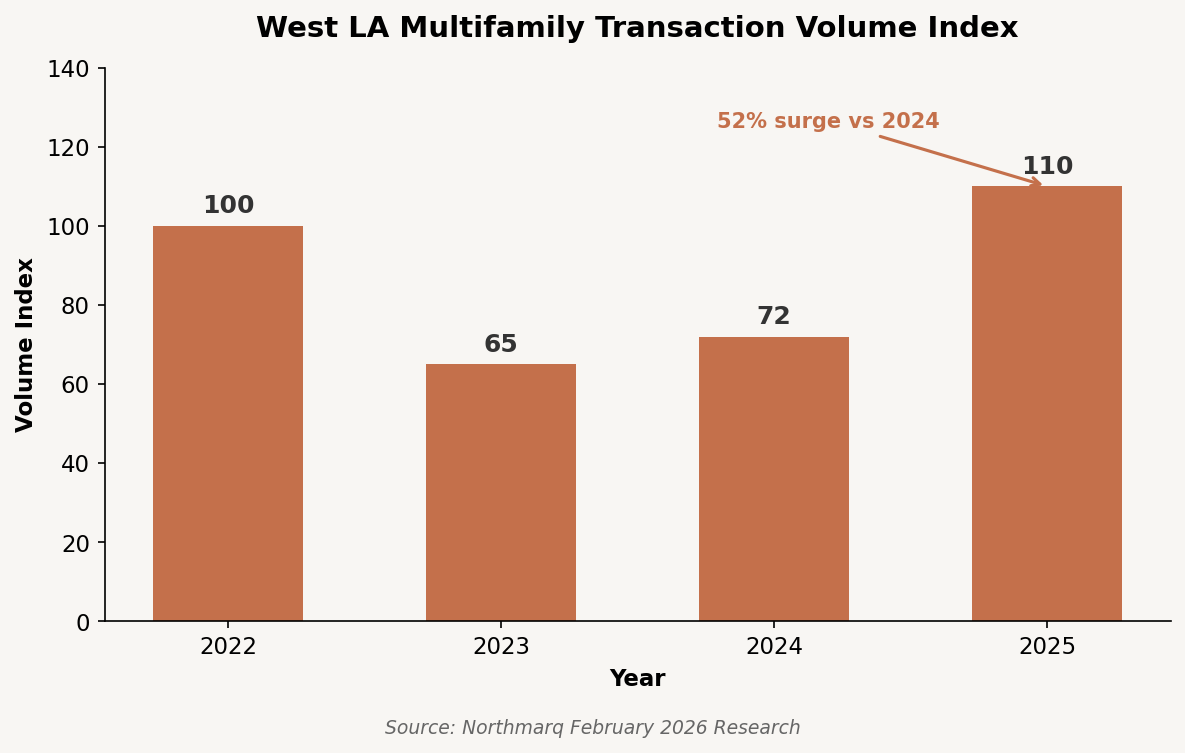

The Case for Moving in 2026

Transaction volume in LA multifamily surged 52% in 2025 versus 2024.[4] Buyers are active. That much is true and encouraging.

But the argument for selling in 2026 is not that things are great. It is that several headwinds are building simultaneously. They are easier to exit in front of than to wait through.

Rents declining. Record supply coming. RSO growth ceiling reduced. Financing costs elevated. Buyers are pricing all of that in right now. They are not fully pricing in what another year of the same conditions looks like. That gap between current buyer pricing and where pricing goes if you wait. That is the window.

The median price per unit metro-wide sits at $311,600, down approximately 2% year over year.[4] Prices are softening modestly. Owners who wait for a recovery may be waiting through more softening instead.

For perspective on how to think about sale timing, read When Is the Right Time to Sell Your Apartment Building.

To understand exactly what your building is worth in Q1 2026, request a complimentary broker opinion of value. No obligation. Just the numbers, based on where the market actually is today.

Talk to Someone Who Has Been in the Room

I am not summarizing reports. I am writing the offers. If you own a building on the Westside and want a straight answer on what it is worth in this market, call me.

Don Favia President, Favia Investment Group Realty Investment Advisors | DRE #01841258 424-377-6002 | dfavia@realtyinvadvisors.com Learn more about our Westside multifamily practice

Sources

[1] Kidder Mathews, Los Angeles Multifamily Market Research Q4 2025, kidder.com

[2] GlobeSt, LA Multifamily Demand Turns Negative as Construction Remains Robust, January 16, 2026, globest.com

[3] Matthews Real Estate Investment Services, West Los Angeles Multifamily Market Report Q4 2025, matthews.com

[4] Northmarq, Apartment Demand Reaches Three-Year High in Los Angeles Multifamily Market, February 2026, northmarq.com

[5] ApartmentList / Santa Monica Daily Press, Santa Monica Rent Report, March 2026

[6] Realty Investment Advisors internal pricing intelligence, based on closed Westside transaction data, updated March 2026

[7] CRE Daily / RealPage Market Analytics, Los Angeles 2026 Apartment Deliveries, 2026

[8] AAGLA, LA RSO Ordinance Revision, effective January 24, 2026 / July 1, 2026

[9] CNBC, Fed Holds Key Interest Rate Steady as Economic View Improves, January 28, 2026, cnbc.com

[10] CNBC, As Iran War Heightens Affordability Issues, Don't Expect the Fed to 'Ride In and Save the Day', March 12, 2026, cnbc.com

[11] Goldman Sachs, The Outlook for Fed Rate Cuts in 2026, goldmansachs.com

About the Author

Don Favia is President of Favia Investment Group, operating under Realty Investment Advisors (DRE #02063191). With 20 years of multifamily investment sales experience, he has closed over $370M in transactions across 100+ deals and 850+ units, specializing in Santa Monica, West LA, Mar Vista, Westwood, and the broader Westside market.

Disclaimer: This is for general informational purposes only and should not be considered legal, tax, or financial advice. Market data reflects conditions as of March 2026 and is subject to change. Consult with your CPA, tax advisor, and/or attorney for guidance specific to your situation.